BlogTuesday, December 27 2022

Florida Gov. Ron DeSantis signed a sweeping property insurance bill on Friday. How much and when it will work to stabilize the stormy market are among the questions being asked. One of the key goals of the legislation is to keep the claims process from ending up being settled in courtrooms, a problem that DeSantis said drives up legal costs for insurers. “This bill reins in the incentive to litigate,” DeSantis said before signing the bill in Fort Myers, an area devastated by Hurricane Ian in September. “This is going to make a huge, huge difference.” Florida has struggled to keep the insurance market healthy since 1992 when Hurricane Andrew flattened Homestead, wiped out some insurance carriers and left many remaining companies fearful to write or renew policies in Florida. Risks for carriers have also been growing as climate change increases the strength of hurricanes and the intensity of rainstorms. But beyond being prone to hurricanes, Florida needs to reduce legal costs for insurers, DeSantis said. “Florida’s property insurance market was very good for lawyers. Very good. It’s made a lot of people very, very rich. But the question is, is that in your best interest to have a situation like that? And I don’t think it is,” DeSantis said. The Bill Signed by Governor The draft of the measure was revealed Friday evening, Dec. 9. By Tuesday, Dec. 13, the full Senate voted mostly along party lines, 27-13, to endorse it, with no amendments. On Wednesday, the House approved it 84-33. Most provisions will take effect immediately upon the signing of the bill into law.Lawmakers and insurance groups cautioned that it could still be another two years before remedial effects of the legislation are fully realized. The new law will create a $1 billion reinsurance fund, put disincentives in place to prevent frivolous lawsuits and force some customers to leave a state-created insurer of last resort, Citizens Property insurance, for a private insurer, even if the policy costs more. It will also set more stringent deadlines throughout the claims process to try to insure homeowners don’t face coverage delays. Mimi Bright of Parkland said she isn’t expecting relief for policyholders any time soon, but she’s glad that lawmakers are addressing the subject.

“So much for protecting the consumer, right?” Bright said. Average annual premiums have risen to more than $4,200 in Florida, which is triple the national average. About 12% of homeowners in the state don’t have property insurance, compared to the national average of 5%, according to the Insurance Information Institute, a research organization funded by the insurance industry. Insurance Losses The insurance industry has seen two straight years of net underwriting losses exceeding $1 billion in Florida. Six insurers have gone insolvent this year, while others are leaving the state. But Democrats opposed the bill, saying it doesn’t do anything to help stop huge rate increases and cancellations that homeowners are struggling with. The legislation will remove “one-way” attorney fees for property insurance, which require property insurers to pay the attorney fees of policyholders who successfully sue over claims, while shielding policyholders from paying insurers’ attorney fees when they lose. It will also eliminate the state’s assignment of benefits laws, in which property owners sign over their claims to contractors who then handle proceedings with insurance companies. The bill would force people with Citizens policies to pay for flood insurance and require moves to private insurers if they offer a policy up to 20% more expensive than Citizens. Citizens recently topped 1 million policyholders for the first time in a decade. In a plus for consumers, it will also speed up deadlines for insurance companies to respond to and act on claims. To help at a time when companies are slammed with claims, the law allows insurers to begin the claims process through video, photos and teleconferences rather than sending an agent to every damaged property. The new law comes as Insurance Commissioner David Altmaier steps down from his position. DeSantis said Friday the position has already been posted. DeSantis also signed a bill to provide property tax rebates to people whose homes were left uninhabitable by Ian. The bill also provides money for recovery. Wednesday, December 21 2022

Earlier this week, Florida’s Legislature approved the boldest and most comprehensive property insurance reforms in decades. This morning, Governor Ron DeSantis signed SB 2A in Ft. Myers Beach, surrounded by Florida’s legislative leaders, the bill’s sponsors, and insurance consumers. Senate Bill 2A addresses a wide variety of topics, including: Reinsurance Senate Bill 2A creates the Florida Optional Reinsurance Assistance (FORA) Program within the Florida Hurricane Catastrophe Fund (FHCF). The FORA Program provides four layers of optional reinsurance at “reasonable rates” (50–65 percent rate online), starting at the FHCF attachment point and proceeding downward. Claims Filing Deadline Senate Bill 2A reduces the claims filing deadline from two years to one year of the date of loss for new or reopened claims. The bills provide 18 months for supplemental claims. Office of Insurance Regulation (OIR) Regulations Senate Bill 2A provides additional authority to the OIR to subject any authorized insurer to a market conduct examination. Insurance Company Duties Senate Bill 2A amends the prompt-pay statutes to ensure timely claims handling. This is accomplished by:

Attorney Fees Senate Bill 2A repeals the one-way attorney fee statutes for litigated property (commercial and personal lines) insurance claims. The bill also provides other legal reforms addressing abusive litigation tactics. Assignment of Benefits Senate Bill 2A prohibits the use of assignment of benefits, in whole or in part, of any post-loss insurance benefit under any property (commercial and personal lines) insurance policy issued on or after January 1, 2023. Citizens Reforms Senate Bill 2A includes several provisions addressing the growth and exposure of Citizens. Additionally, SB 2A provides a phased-in flood requirement for Citizens’ policyholders. These provisions include:

Continuation of Coverage The Legislature included a provision that provides the insurance commissioner discretion to extend the 30-day cancellation period of policies of an insolvent insurer to 45 days to provide more time for agents to replace coverage for consumers. Tuesday, December 20 2022

After years of what some insurers have labeled half-measures, Florida lawmakers appear to be on the cusp of delivering “historic” and “transformational” reforms that would end one-way attorney fees, banish assignments of benefits and offer state-backed reinsurance at a discount. House Bill 1A and Senate Bill 2A were posted late Friday, just three days before a special legislative session that begins today. The bills were met with widespread applause from insurance industry leaders, attorneys and consultants. “The proposed legislation sends a strong message that Florida is serious about stabilizing the property insurance market and creating an environment to attract capital and create more options for Florida’s insurance consumers,” the Florida Association of Insurance Agents said in a statement. After nine insurer insolvencies in the last three years and spiking premiums across the state, the bills aim to tackle the major cost drivers, including the incentives behind what insurers have dubbed runaway claims litigation. They also would address other cost factors and provide some consumer protections that would force insurers to pay or deny claims more quickly, to be more judicious about demanding the appraisal process in claims disputes, and face new scrutiny from regulators. An attorney who represents property owners said the proposals take away policyholders’ rights and eliminate longstanding safeguards designed to level the playing field between insureds and well-heeled insurance companies. Here’s a look at the bills’ proposed changes: Mandatory Flood Insurance for Citizens’ Insureds The measures would require policyholders of the state-created Citizens Property Insurance Corp. to also purchase flood insurance. The bills provide a timetable for phasing in the requirement, with more expensive properties needing it first, by March 1, 2024. All policies would need flood insurance by March 2027, regardless of the property’s elevation or location. The idea was discussed in the Capitol in the mid-2000s but never gained traction. Now its time has come, said Scott Johnson, a longtime insurance consultant and educator who recently broached the possibility of reviving it. “I was surprised that’s in the bill now,” Johnson said Sunday. He has argued that insureds who receive payouts on water losses after a storm are less likely to file suit over whether the damage was from wind or floodwaters, which could help reduce Citizens’ staggering litigation defense costs. “Most of the people in Citizens are probably candidates for flood insurance and it’s really just a prudent way to make sure claims can get paid, because in the end, a lot of those claims were not wind claims, they were flood claims,” said Fred Karlinsky, an insurance defense attorney and lobbyist for the industry. The 20% Rule The bills also revive a plan that would essentially force Citizens’ policyholders to switch to a primary market carrier if that carrier’s premiums are no more than 20% higher than Citizens’, upon renewal. Citizens’ premium increases are limited by law – the main reason the insurer has become the largest carrier in Florida, with some 1.2 million policies in force. A similar provision was included in SB 1728, which was approved by the state Senate in the regular 2022 legislative session. The bill died when the House did not approve it before the 60-day session came to a close. The new bill also would allow Citizens to combine its three accounts (personal lines, coastal and commercial) into one. That would let Citizens access its entire surplus to pay claims and would limit the potential surcharge or assessment on policyholders – from one charge per account to a single surcharge, if the corporation runs a deficit. Expansion of Arbitration The bills would codify what a few insurers have already adopted: binding arbitration clauses. Insurance carriers would not be allowed to require arbitration as an alternative to litigation unless it is clearly explained in a separate policy endorsement, the insured is offered a premium discount in exchange, and the policyholder signs a form accepting the clause. One-way Attorney Fees On the biggest cost drivers, insurers have said for years, is Florida’s claimant-friendly one-way attorney fees statute, which requires insurers to pay the plaintiffs’ legal fees if the carrier loses in court. The law has been in effect, in one form or another, since 1893, and is more akin to the English rule of law, according to a legislative staff analysis of the newly drafted bills. In 2016, a famous Florida Supreme Court decision underscored the legitimacy of the practice. That, along with fee multipliers, have caused fees to explode in recent years and has been the incentive behind Florida’s out-of-control claims litigation industry, insurance advocates have said. HB 1A and the nearly identical SB 2A address legal fees head-on, stating flatly that the one-way attorney statute shall not apply to insurance claims litigation. A court could award fees to the prevailing side after a dispute is adjudicated, the bill’s sponsor explained in a Senate committee meeting Monday. Assignments of Benefits The bills also would prohibit AOBs for residential and commercial claims, a move that a growing number of insurance executives have called for. Assigning benefits to restoration companies is one of the biggest cost escalators because it gives contractors an unnatural incentive to inflate estimates and scope of repairs, critics have said. And when insurers balk at the claims, the assignees are often quick to sue. Bad-faith Litigation For years, insurance defense attorneys have argued that Florida’s statutes make it too easy for plaintiffs to file bad-faith actions against insurers, long before a case has been fully adjudicated and even if claims have been paid. The special session bills would bar bad-faith claims until after a court has decided that the insurance company breached the policy contract. Faster Action on Claims The proposed legislation would cut the time allowed for insurers to pay or deny claims, from 90 days to 60. The Florida Office of Insurance Regulation could extend the time in states of emergency or if the insurer suffers a cyber attack or other computer system failure. The bills also reduce the time that insurers have to review and acknowledge a claim communication, from 14 days to a mere seven. Inspections would have to be done in 30 days, even after a hurricane. All of that could force insurers to hire staff to meet the new demands, or at least to become more efficient. Insureds also would have less time. Instead of two years, as was required in 2021 legislation, policyholders would have only one year after the date of the loss to file new or reopened claims. For supplemental claims, the deadline would be shortened from three years to 18 months. More Regulatory Scrutiny Insurers that unjustly compel claimants to turn to the appraisal process could have their certificates of authority suspended, face fines from the OIR, and be publicly named and shamed on the OIR website, the bills note. The staff analysis of the bills did not explain what prompted the section, and its inclusion surprised some industry insiders. Insurers have said the appraisal process can provide a fair method method to determine the cost of damage to a property, with the use of three independent appraisers. But a plaintiffs’ attorney said that some property insurers have abused the process by underpaying a claim, then immediately invoking the appraisal route, which delays resolution and adds expense for insureds. “This practice ignores the obligation to adjust the loss with the insured and instead allows an insurance company to avoid its duties to try and resolve the claim,” said Gina Clausen Lozier, a plaintiffs attorney in West Palm Beach. “The appraisal process often requires an insured to incur additional costs for appraisers and an umpire which may have been unnecessary if the insurance company had taken the opportunity to properly adjust the claim with the insured.” Karlinsky said he didn’t know if appraisals had become such an issue. “I think the Legislature wants to put some guardrails around things and we understand the need to do that,” said Karlinsky, who, as a registered lobbyist, has represented almost two dozen insurers in recent years. Under the bill, OIR also would have new authority to require more information in insurers’ quarterly reports, which currently includes policy counts, premium written and exposure by county. Many insurers have claimed that such data is considered “trade secrets,” leaving an incomplete picture for stakeholders, regulators and the public, critics have said. Regulators also would be able to subject insurers to a market conduct examination after a hurricane, the bills note. The legislation, if signed into law, also would provide OIR with an extra $1.76 million per year to hire new staff to keep up with its new responsibilities. The move may address concerns that some lawmakers expressed at the May special session, that OIR was understaffed and was not aggressive enough in bird-dogging struggling insurance companies. Low-cost Reinsurance Crucially, the FAIA leadership and others said, SB 2A and HB 1A would provide a new layer of state-funded reinsurance – at a significant discount from what the market offers. Reinsurance prices for Florida property carriers have soared by more than 80% in recent years and are expected to rise again in 2023, according to market reports and the bill analysis. Those costs have been a significant factor behind several recent insolvencies, troubled carriers have said. The bills would establish the Florida Optional Reinsurance Assistance Program, or FORA. The coverage would begin at the Florida Hurricane Catastrophe Fund’s attachment point, currently at about $8.5 billion for the industry, and would cover up to $5 billion in losses below that. Rates would range from 50% to 65% lower than private reinsurance market rates. It would be funded with $1 billion in state funds and from premiums paid by participating insurance companies. The less-extensive Reinsurance to Assist Policyholders (RAP) fund, established at the May special session, would continue for at least another year. FAIA President Kyle Ulrich said the new program will help stabilize the Florida property insurance market. Karlinsky said lawmakers are using the tools they have, but that the FORA plan may not go far enough. What the Bills Don’t Address Somewhat surprisingly, the measures do not address two elements that public officials and insurers have said are crucial to putting the brakes on claims litigation and outsized loss adjustment expenses: limits on public adjusters, and on ways to make it easier for insurers pay actual cash value, as opposed to replacement value, for damaged structures. Florida’s chief financial officer, Jimmy Patronis, and others have said that southwest Florida was practically overrun with public adjusters just days after Hurricane Ian damaged thousands of homes in the area, and he called for slashing fees that adjusters can charge and for more prosecutions of those who violate the law. “Florida’s problem won’t be completely solved until you get public adjusters out of there,” Johnson said. The actual-cash-value issue was partly addressed in May, when lawmakers revised statutes that had required full replacement of roofs when only small parts were damaged. The Session The new bills, some of the first to be considered by the newly elected 2023 Legislature, were said to have been drafted by House and Senate leadership, with input from the Florida governor’s office. But industry insiders pointed out that state Sen. Jim Boyd, R-Bradenton, the longtime chair of the Senate Banking and Insurance Committee and an insurance agent himself, is the sponsor of SB 2A and likely crafted most of the bill language. Boyd was instrumental in crafting the two bills that moved quickly through the May special session. And if next week is anything like that session, the bills will see few changes in committee or on the floor. With Republicans having a larger majority now than in May, the measure are expected to sail quickly through the chambers, with a final gavel as soon as Wednesday. Both chambers convene today at 10:30 a.m. and Senate committee meetings start at noon. The FAIA cautioned stakeholders not to expect an immediate improvement in insurers’ finances or a rapid drop in insurance premiums. Karlinsky noted that whatever reforms are passed this week, they will probably be challenged in court by contractors and trial lawyers, a process that could take a few years to resolve. “I would applaud the Legislature and the governor for trying to fix something that has been plaguing Florida citizens for too long, and hopefully this will stem the tide of some of the ills we have faced for many many years,” Karlinsky said, calling the proposed legislation “pretty transformational.” Thursday, December 15 2022

Ahead of this week’s special legislative session in Florida, the AM Best financial rating firm predicts that “without immediate and substantive long-term legislative reforms,” further insurer insolvencies are on the near-term horizon. “The outcome of the special legislative session could affect the capital allocation strategies of reinsurers that have to decide where to invest their dollars in the coming year,” according to David Blades, AM Best associate director for industry research and analytics. Counting six insurers declared insolvent already since late February, the commentary, “Florida Government Seeks to Repair Property Insurance Market,” highlights declining capacity in a state trying to recover from Hurricane Ian, and the mushrooming size of the state-backed Citizens Property Insurance Corp. Rising Florida claims costs aren’t just attributable to catastrophe exposures in the state, but also to a highly litigious Florida environment. “This higher risk and higher cost environment needs to be considered to ensure there are dollars available to pay insurance claims. Without changes to reduce the costs in the system and better manage the impact of catastrophes, further insolvencies are likely,” AM Best analysts wrote in the commentary. The state is now depending on Florida specialist carriers, which are especially vulnerable given their weaker balance sheets (compared to national carriers) and overreliance on reinsurance for balance sheet protection and short-term capital. The special legislative session that began today, Dec. 12, will seek to implement long-term reforms to address challenges posed by one-way attorneys’ fees, assignment of benefits (AOB) issues and roof coverage reforms to help stabilize Florida’s property insurance market. “AM Best views long-term solutions as the only way to attract large national players, as well as new capital, back to the market in earnest; however, carriers are unlikely to take such a step until necessary reforms have taken hold and once prevailing rates are sufficient to cover the risks they must bear,” the report says. “Public policy initiatives need to consider how to make Florida attractive to national insurers and reinsurers, to incentivize them to expand their appetite for Florida risks,” said Sridhar Manyem, director, industry research and analytics, AM Best, in a media statement announcing the commentary. “Absent that, a lack of competition may continue to fuel affordability issues for primary insurers with respect to reinsurance and consumers in need of basic homeowners’ coverage.” Blades added: “Although claims stemming from Hurricane Ian at this point are lower than that of 2017’s Hurricane Irma, the rising reinsurance costs could reach a breaking point for many primary insurers in June 2023, when Florida property-catastrophe reinsurance programs are scheduled for renewal.” The report describes reforms signed into law this year following a May 2022 special session. Those included establishment of the “Reinsurance to Assist Policyholders” (RAP) program. The RAP provides $2 billion of reinsurance coverage to insurers at no cost in exchange for lower premiums for policyholders. Sitting below reinsurance coverage from the Florida Hurricane Catastrophe Fund, the RAP coverage is available in the event of a hurricane, the report says. AM Best adds that while the rate reduction requirement may provide some relief for consumers, it does not address rate inadequacy issues driven by litigation, worsening weather activity, and escalating reinsurance pricing. Other reforms passed at the May session prohibited awards of attorneys’ fees to an assignee in AOB litigation, and curbing the use of contingency fee multipliers in fee awards. Both fell short of repealing a one-way attorney’s fee rule in the state (which permits policyholders filing lawsuits to recover legal costs when they prevail in court but prohibits insurers from doing the same). Echoing what many insurers and defense attorneys have said for years, AM Best described the one-way rule as “the driving force of behind the litigation crisis in Florida.” Reinsurers have shown by their actions that they don’t think piecemeal measures will have a significant impact on social inflation. “Some reinsurance companies have decided to drastically reduce their property cat exposures in Florida by shifting towards higher attachment points, lowering limits, and being more selective with respect to their cedents’ track records—despite a hardening market, with rate increases in the double digits,” the report reads. Thursday, December 08 2022

A list of potential fixes await Florida lawmakers next week during yet another special legislative session aimed at stabilizing the state’s insurance market. But before enacting any reforms that could quell spiraling property insurance premiums, lawmakers will hear impassioned arguments by advocates for private insurers and their adversaries — repair contractors and the plaintiffs’ attorneys who represent them. Senate President Kathleen Passidomo, R-Naples, and House Speaker Paul Renner, R-Palm Coast, released a formal session proclamation Tuesday scheduling the special session from Monday to Dec. 16. While bills have not yet been filed, the proclamation lists seven insurance-related topics for consideration and three others that would provide relief to consumers and victims of hurricanes Ian and Nicole. According to the proclamation, the Legislature will consider reforms that would:

Two other goals not directly related to the insurance industry would provide tax relief and other financial help to victims of hurricanes Ian and Nicole, provide additional ways to support disaster response, recovery and relief efforts by the state Division of Emergency Management, and establish a statewide toll credit program for frequent Florida commuters. Even before specific legislation has been filed, representatives of the two major interest groups — insurers and trial lawyers — that would be affected by reforms have begun making their cases to the public. At the Florida Chamber’s annual Insurance Summit in Orlando on Tuesday, insurance industry insiders called for legislation they hope would end or sharply curtail practices they say have led to spiraling costs, high homeowner premiums, and the nation’s highest rate of claims litigation. Currently Florida is responsible for 7% of the nation’s insurance claims and 76% of its property insurance lawsuits, according to data compiled by the National Association of Insurance Commissioners. Insurers have posted five straight years of collective operating losses and were poised to lose $1 billion in 2022 before Ian and Nicole hit the state. The two storms caused $1.2 billion in losses in the third quarter alone, Citizens President and CEO Barry Gilway reported. Meanwhile, six insurers were declared insolvent prior to the storms and another, St. Petersburg-based United Property & Casualty, was placed under administrative supervision by the state Office of Insurance Regulation on Monday after reporting a $173 million net loss in the third quarter. The order requires the company to wind down operations before the 2023 hurricane season begins on June 1. Policyholders displaced by carriers’ insolvencies and financial losses have had little choice but to buy coverage from Citizens, the state’s insurer of last resort. Citizens’ policy count has increased from 708,000 in 2021 to 1.13 million now, and Citizens projects it will increase to 1.68 million by the end of next year. Lawmakers and industry officials have long expressed concerns that Citizens could grow too big, exposing nearly all insurance customers in the state to special assessments if the company is unable to pay claims after a series of major storms. Curtailing Citizens’ growth requires strengthening the private insurance market by reducing incentives to sue carriers, summit participants said. One incentive insurers want eliminated is the so-called “one-way attorney fee” law. Insurers say the law encourages litigation by awarding legal fees when claims disputes are settled for any amount, even $1, over insurers’ original offers. The “one-way” moniker stems from the fact that homeowners named in suits against insurance companies aren’t required to pay insurers’ legal fees if their lawsuits do not succeed. That encourages attorneys to try to overwhelm insurers by filing multiple lawsuits, even over the same claim, in the expectation that they will settle instead of incurring costs of prolonged litigation, insurers say. David Altmaier, Florida’s insurance commissioner, said he expected the Legislature to repeal the state’s “one-way attorney fee” law next week. “Now is as good an opportunity we’ve ever had to do this,” he said during a panel discussion at the summit. He later added, “It looks like we’re probably going to be there this session.” Insurers are also hopeful that the Legislature will agree to further restrict the ability of policyholders to sign over benefits of their insurance claims to third-party repair contractors. Contractors use assignments of benefits (AOBs) to stand in homeowners’ shoes and sue insurance companies in policyholders’ names, insurers say. Armed with AOBs for roof damage and non-weather-related water claims, contractors submit inflated invoices and sue when insurers underpay or refuse to pay them, insurers say. AOB reforms enacted in recent years have curtailed but not stopped abuses, insurers said. Christine Ashburn, chief of communications, legislative and external affairs for Citizens, said that although a previous reform reduced availability of attorneys’ fees in lawsuits involving AOBs, “we’re still seeing three to four AOBs per claim.” At resource centers set up to connect homeowners with their insurers, contractors were handing out business cards to crying residents “who hadn’t even been back to their homes,” she said. Ashburn said the solicitations “proved our point” and added, “We just think AOBs need to go away. Just forget them.” Plaintiffs’ attorneys, however, say their services would not be needed if insurers paid claims in full and on a timely basis. A YouTube video uploaded by attorney Steven Bush and shared widely by plaintiffs’ attorneys on Monday accused unnamed insurance companies of fraudulently changing damage estimates prepared by insurance adjusters after Hurricane Ian. Three adjusters interviewed in the video said insurers reduced the scope of damages on the estimates without their knowledge or consent, yet left the adjusters’ names on the estimates. In one example, an adjuster said his full-roof replacement estimate was altered by an insurer to make it appear that he recommended replacement of only 498 tiles. Commenting by email about the upcoming special session, Maitland-based attorney Imran Malik said, “The current narrative seeks to portray lawyers as the problem when in reality we are only hired because an insurance company is not paying what they are contractually obligated to do.” Next week’s session will be the second this year to deal with the insurance crisis. In May, concerns that many private companies were not healthy enough to secure needed reinsurance before hurricane season prompted the Legislature to create a $2 billion taxpayer-funded reinsurance fund to supplement private reinsurance and the state’s Hurricane Catastrophe Fund. Legislators are expected next week to consider making more reinsurance capital available to keep vulnerable companies afloat until reforms begin reducing losses. Yet, global providers of reinsurance capital remain reluctant to invest in Florida companies without reforms to reduce litigation, said Joanna Syroka, senior underwriter and director of new markets at Fermat Capital Management LLC, a Connecticut-based investment management firm specializing in insurance-linked securities. She noted that reinsurers used traditional loss expense modeling to project that losses from 2017′s Hurricane Irma would total $18 billion. But in the five years after Irma, late-filed claims and legal costs — known euphemistically as “social inflation” — drove those losses up by another $12 billion. The additional losses have triggered a “loss of trust” in Florida among reinsurers, she said. Now, she said, “all eyes are on Hurricane Ian,” with projected losses of $41 billion, Syroka said. “Will we see another $10 billion in social inflation? Will it be more? Will it be less? At this stage, we need evidence that these [proposed] changes will make a difference.” Thursday, December 08 2022

Getting insurance coverage from state-owned Citizens Property Insurance Corp. could become more expensive if state lawmakers agree that the company’s artificially low rates are hurting Florida’s private insurance market. Citizens wants to be the insurer of last resort, and not the insurer with the lowest premiums. Homeowners have turned to Citizens over the past three years as spiraling losses have forced private market companies to fold, raise rates, and stop writing new business in the state. Since 2019, Citizens’ policy count has increased from about 420,000 to 1.13 million, and Citizens projects it will increase to 1.68 million by the end of next year. Company leaders are hoping that the Florida Legislature, during a special session on insurance issues scheduled next week, will consider measures that would make the company less financially appealing to customers and compel them back to a more-expensive private company. A proclamation announcing the special session listed, among numerous goals, an intention to enact reforms that would “foster the transition” of Citizens policies to the private insurance market. Officials have long said the most effective way to accomplish that goal would be to hike Citizens’ costs. No specific bills have been filed for the special session, but Citizens officials acknowledged Wednesday that they have had discussions with leaders of the state House and Senate and governor’s office to convey what they would like to see enacted. Barry Gilway, Citizens’ president and CEO, on Wednesday told the company’s Board of Governors that Citizens’ average premium of $3,227 is 44% lower than the $5,788 average that the private-market customer pays. “We’re not a residual [last-chance] market, we’re competing openly with the private marketplace. We don’t want to, but we are,” Gilway said. Later he added, “The reality is we are ridiculously competitive and we need relief relative to overall rates.” In 2021, average Citizens premiums were 36% lower than the private market. The spread was wider in counties north of the South Florida metro area — more than 50% less in Pinellas or Pasco counties, he said — and “maybe” 20% lower in Broward and Miami-Dade counties. “You’ve got insureds who are coming to us from insolvent insurers and we’re saying, ‘Welcome, here’s a 30% discount.’” Gilway called for a “fundamental fix” that would bring Citizens’ rates close to what’s known in insurance circles as “actuarial soundness” — which means what a normally functioning company would need to charge in the private market to pay off all claims, cover overhead and make a small profit. But Citizens isn’t a normal company, and it’s been providing artificially low rates since at least 2007, when then-freshly elected Gov. Charlie Crist convinced the legislature to temporarily freeze Citizens rates. In 2009, Crist and the Legislature ended the freeze but enacted a new law that prohibited average annual rate increases of more than 10%. Prior to the price freeze, Citizens’ rates were calculated using a formula designed to ensure they remained more expensive than the 20 largest private market insurers. The formula was intended to prevent Citizens’ rates from becoming too attractive to homeowners, and to keep the company as the insurer of last resort. Instead, the 10% rate cap drove Citizens’ rates lower as private market companies were allowed to raise rates 20%, 30%, 40% and more. Citizens can keep rates artificially low because, among other reasons, it’s not required to turn a profit on operations and is able to generate income off of its $4.4 billion surplus, which was $6.8 billion before factoring in $2.4 billion in losses from Hurricane Ian this fall. In 2021, Gov. DeSantis signed a bill allowing Citizens to increase the rate cap each year from 10% by an additional 1% a year over five years. The first increase, to 11%, took effect on Aug. 1 and the second hike to 12% will take effect on Jan. 1. But the Florida Office of Insurance Regulation in June rejected a bid by Citizens’ Board of Governors to raise all customers’ rates by the new maximums, saying their methodology for determining those increases differed from historical norms that required rate decreases for some customers where warranted. During Wednesday’s meeting and at a Florida Chamber-sponsored insurance summit the previous day in Orlando, Citizens officials signaled that they haven’t given up trying to persuade the Legislature to enact measures that would increase the company’s rates. “I do believe Citizens will be on the table next week,” said Christine Ashburn, the company’s chief of communications, legislative and external affairs, at the insurance summit on Tuesday. Which ideas might emerge for debate during the session — and how many lawmakers would be willing to vote for ideas that would increase, and not lower, homeowners’ insurance rates — remains to be seen. Gilway mentioned pitching two specific reform proposals but said he had no idea whether any would show up in bills to be filed for the session, which begins Monday. Citizens officials mentioned several ideas on Tuesday and Wednesday that have been previously raised but not enacted:

Tightening eligibility thresholds, Ashburn said at the summit, would encourage investment in private-market companies. Reforms would create a large pool of eligible customers with no pending litigation or open claims for private companies to take out and rely on to build a profitable book of business. Tuesday, December 06 2022

Hurricane Ian didn’t break Florida’s property insurance market. Insurers have the capacity to pay claims from the storm, which struck Southwest Florida last month as a Category 4 hurricane that destroyed hundreds of structures and killed more than 100 people. Losses estimated by domestic insurers have been readjusted this week to levels lower than originally estimated and experts say those losses will remain well within companies’ abilities to pay claims. They’ll be doing so out of their surpluses and reinsurance they were able to secure before this year’s hurricane season. That’s the good news. The bad news is that numerous insurance experts predict that the state legislature will need to take more action to shore up the industry before the 2023 hurricane season, possibly by pledging more public funding to ensure companies can maintain required funding levels. Ian is still expected to be one of the nation’s costliest storms ever and will increase costs of reinsurance — that is insurance that insurers buy — before the next two rounds of reinsurance renewals on Jan. 1 and June 1. And those higher costs will be absorbed by homeowners across the state next year, regardless of whether they were unfortunate enough to live in Ian’s path or in a part of the state that emerged relatively unscathed, as South Florida and the Panhandle did. “Everyone is going to have to pay some increase,” says Paul Handerhan, president of the Federal Association for Insurance Reform, a consumer-focused watchdog group that advocates for legislative changes that it sees as necessary to keep insurance available and affordable in the state. How much more we’ll be paying next year remains to be seen. But it will be yet another punch in the pocketbook for homeowners who have seen their insurance premiums roughly double over the past five years to about three times the national average. Average annual premiums this year topped $4,000 in five Florida counties, including Broward, Palm Beach, Miami-Dade and Monroe, state data shows. Projected losses less than fearedEstimates for Ian’s insured losses are wide ranging, from a low of $30 billion to more than $75 billion. Stonybrook Capital recently said that Ian could cost $75 billion or more, making it the third-most expensive insured event in U.S. history, behind only the terrorist attacks of Sept. 11, 2001 and 2005′s Hurricane Katrina. Catastrophe modeling firm Karen Clark & Co. projects insured losses of $63 billion, except for flood losses covered by the National Flood Insurance Program. Analytics firm RMS projects insured losses will land somewhere between $53 billion and $74 billion, excluding NFIP-covered flood losses, companies’ loss adjustment expenses, auto and marine losses and inevitable costs of litigation. Several domestic insurers, including publicly traded Heritage Property & Casualty, Universal Property & Casualty, and Homeowners Choice, have released statements projecting that their losses won’t exceed their abilities to cover them out of of their surpluses and available reinsurance. Stacey Giulianti, chief legal officer at Boca Raton-based Florida Peninsula Insurance, says insurers have reduced loss estimates after two weeks of damage inspections along Ian’s path. One reason is that despite Ian’s deadly storm surge, its actual hurricane-strength wind field had a much tighter radius than other recent storms, Giulianti said. After destroying structures in Fort Myers Beach, Cape Coral and low-lying parts of western Fort Myers, the storm’s winds rapidly weakened as moved over sparsely populated agricultural and preserve land. “Virtually every carrier has slashed their projected ultimate losses by a huge percentage,” Giulianti said. “Reinsurance will cover this storm easily for domestic carriers with plenty of room to spare should a late season cyclone threaten the peninsula. Except for the first 24 hours after landfall, we have seen claim reports drop dramatically and have had essentially zero telephone wait times in our claims department. “This storm is unlikely to knock out any conservative insurance carriers that have sophisticated reinsurance towers and ample surplus.” State-owned Citizens Property Insurance Corp., the insurer of last resort, has revised its Oct. 5 projection for total number of claims from more than 225,000 to 100,000. “We initially estimated that damage and claims numbers would be far greater outside of the three-county area of Lee, Charlotte and Sarasota counties than we are seeing at this point,” spokesman Michael Peltier said. Its projected loss estimate remans at $2.3 billion to $2.6 billion “until we can base it on actual losses,” Peltier said. If losses remain at those levels, CItizens won’t have to recover any shortfall from its own policyholders or from insurance consumers statewide with levies or special assessments. Florida’s Hurricane Catastrophe Fund, which provides reinsurance that companies can tap after exhausting their privately funded reinsurance, could be forced to pay between $10 billion and $12 billion of its $17 billion claims-paying capacity, says Locke Burt, chairman and CEO of Ormond Beach-based Security First Insurance Co. That would have to be replenished but can be done so over several years, through the fund’s purchase of long-term bonds and ability to levy surcharges on private-market policies. Flood losses from Ian’s storm surge were estimated by CoreLogic at between $8 billion and $18 billion for residential and commercial properties. Uninsured flood loss is estimated to be between $10 billion and $17 billion. But those losses won’t impact Florida property and casualty insurers because flood insurance is covered by the National Flood Insurance Program and private carriers. Reinsurance will be harder to getEven before Ian hit, Florida insurers struggled to buy enough reinsurance to guarantee their ability to pay claims after two major storms, including a 1-in-130-year hurricane that has never before happened. The closest was the Great Miami Hurricane of 1926 that caused the equivalent of $235 billion in damages and killed 372 people. Six insurers went insolvent this year, in part because they didn’t have enough capital to secure reinsurance levels required by state insurance regulators and Demotech, an Ohio-based agency that assigns financial strength ratings for federal loan guarantors Fannie Mae and Freddie Mac. Those loan guarantors require properties in their portfolios to maintain “A” strength ratings. Reinsurers are typically based overseas, in places like Bermuda, and are unregulated by states or the federal government. That means they can sell as much or as little coverage as they want, factor in whatever risks they fear, and charge anything they want for the coverage. Lately, with severe weather events becoming more frequent and more destructive, Florida insurers have been losing money and reinsurers have been willing to sell less coverage and demanding more money for it, Handerhan said. Reinsurers’ appetite for Florida risk is likely to shrink even further after Ian, largely because Florida’s army of plaintiffs attorneys makes catastrophe risk modeling impossible, industry experts say. While just 9% of the nation’s homeowner insurance claims are generated by Floridians, 79% of all lawsuits against homeowner insurers originate here, the Florida Office of Insurance Regulation has reported, using data from the National Association of Insurance Commissioners. High litigation rates after major storms like 2017′s Irma, a slow-moving storm that caused damage throughout the state, and 2018′s Michael, which hit the Panhandle with Category 5 strength, created greater losses than reinsurers initially estimated. Stonybrook Global’s $75 billion loss estimate, which it says was derived by averaging projections from major catastrophe risk modeling firms, assumed that litigation would increase actual loss costs by another 20%. The firm estimated that Ian will wipe out a year’s earnings for global reinsurers and result in double digit operating losses for domestic companies. Looking forwardThe biggest risk facing property and casualty insurers in Florida will come well after Ian’s debris is hauled away and rebuilding efforts have commenced: How many insurers will be financially healthy enough to secure needed reinsurance for next year’s spring storm and summer hurricane seasons? Like this year, some companies might not be able to raise the needed capital to satisfy Demotech and the Office of Insurance Regulation and will likely go insolvent, Handerhan predicted. “It’s going to be a huge problem. If they can’t get reinsurance, you could see more insolvencies,” he said. Companies strong enough to make the buys will pay more. Last year, most insurers paid 50% more to renew their reinsurance policies, “nearly double other coastal states because of litigation cost risk,” said Mark Friedlander, communications director for the Insurance Information Institute, a nonprofit funded by major national insurers. Another special session?Friedlander says the Florida home insurance market is in crisis “because of manmade issues, not natural catastrophes.” He adds, “Roof replacement claim schemes and excessive litigation have led to the market’s deterioration.” Calls are growing for another special legislative session to finish what lawmakers failed to accomplish during the most recent special session in the spring. Then, lawmakers enacted a number of attempted fixes, including creation of a special $2 billion optional reinsurance fund backed by the state’s general fund. Insurers were also allowed to offer depreciated roof value coverage instead of full replacement value coverage. Insurers say they’ve lost millions because standard homeowner policies require full roof replacements if more than 25% of a roof is damaged. The generous coverage incentivizes roofing contractors to “find” damage and sue insurers for the cost of full roof replacements, insurers say. Another special insurance session could include legislation finally killing Florida’s unique one-way attorney fee statute that insurers blame for the state’s disproportionately high litigation rates. The statute removes most of the risk of suing insurers by requiring insurers to pay all plaintiffs attorney fees if a lawsuit produces a settlement for any amount of money over an insurer’s initial offer, but does not require the plaintiff to pay the insurers’ fee if the insurer wins. Citing similar reforms enacted recently in Texas, proponents say numbers of predatory lawsuits in Florida would drop sharply if plaintiffs had to consider out-of-pocket losses before suing. Such a reform would likely restore profitability to many insurance companies, boost confidence of investors, and increase reinsurers’ willingness to underwrite Florida storm risks. But Handerhan said killing the one-way attorney fee statute would also hurt homeowners’ abilities to get their damages repaired because they would have to pay their attorneys out of their ultimate claim settlement, potentially leaving them unable to pay for their repairs. Amy Boggs, insurance section chair for Florida Justice Association, a trade organization for plaintiffs attorneys, said in an email that litigation rates have already declined 30% as a result of reforms enacted since 2019. “However, there have been zero improvements in the insurance marketplace for consumers, nor a lowering of insurance rates after those reforms.” The association, she wrote, “does not see that further litigation reform will do anything to improve the environment for Florida’s homeowners” and could instead put them in an even worse situation when their insurance company decides to ‘underpay, delay and deny’ payment of meritorious claims.” Yet some insurers say they are already hearing attorneys say they plan to file suit to challenge findings that losses were caused by storm-surge flooding rather than by hurricane winds. On the Fox Weather Channel recently, attorney Andrew Lieb described that strategy, saying, “The question becomes, Did the flood happen because your roof was ripped off and that was a wind issue and not a flood issue? Or did it come from a surge and that’s a flood issue?’” In her email, Boggs said, “We already see finger pointing by insurance companies on wind versus flood due to Hurricane Ian.” FAIR: Two important fixes neededHanderhan said FAIR would like to see a special session focus on two remedies. One would eliminate annual rate-increase caps that were put in place for Citizens policies in 2008 by then-Gov. Charlie Crist. At the time, the caps were intended to protect Citizens customers from insurance cost increases. But as private-market companies have been forced to increase their rates far beyond the Citizens cap, Citizens has become a much-cheaper alternative and an unfair competitor, proponents of eliminating the cap say. The other needed reform, Handerhan said, will be to make more state-backed reinsurance available to ensure private-market carriers can survive until recent legislative reforms take effect in two or three years. One way to make more reinsurance available would be to lower the amount of hurricane losses companies would have to endure before becoming eligible for reinsurance through the state Hurricane Catastrophe Fund. FAIR has argued for such a change over the past three years, saying it would keep costs down by allowing insurers to buy less private-market reinsurance. Another way the state should fund more reinsurance would be to create a larger version of the Reinsurance to Assist Policyholders (RAP) fund that made $2 billion from the state’s general fund available to insurers that had trouble finding enough reinsurance on the private market. How much money should be committed depends on how much would be needed, he said. Flush with cash right now, the state can afford to create a larger reinsurance fund to ensure that the industry and the real estate market survives the next storm season, Handerhan said. John Rollins, former chief risk officer at Citizens and current director of ventures at Texas-based Evans Insurance Group, said he expects Florida’s brightest minds will hash out solutions before the start of the 2023 hurricane season. “Unlike in most states, our insurance leaders also live, work, and employ people here, and we have the best talent on the planet to deal with this challenge,” Rollins said. “Likewise, I think our public sector is well stocked with expertise. As with an approaching hurricane, it’s not time to panic, it’s time to prepare.” Monday, December 05 2022

It hasn’t been made official by the governor’s office, but Florida legislative leaders have set a date for a second special session to tackle property insurance issues – Dec. 12 through Dec. 16. Memos from newly sworn Senate and House leadership show the date coincides with already-planned plenary and organizational meetings for the 2023 regular session of the Legislature, which starts in March. A formal proclamation on the special session is expected this week. The memos did not address what reforms may be on the agenda, but insurance industry lobbyists, news reports and comments from legislative officials suggest that lawmakers may squash one-way attorney fees altogether in claims litigation; may further limit assignment-of-benefits agreements; provide a layer of state-backed reinsurance for carriers; and make some adjustments to the Florida Hurricane Catastrophe Fund, perhaps allowing easier access to the fund’s reinsurance. New House Speaker Paul Renner, R-Palm Coast, last week said he is aiming for “systemic reform” that will shore up the private market and steer policyholders away from the ballooning, state-created Citizens Property Insurance Corp., according to Florida Politics news site. He also did not rule out using tax dollars to provide lower-cost reinsurance for insurers, which are now facing another round of double-digit price increases from private reinsurance firms. Many in the insurance industry have advocated for a lower cat fund retention level, or lower deductible, for carriers, to allow them to access the fund sooner, saving them significantly on reinsurance costs. But after Hurricane Ian hit Florida in September, the cat fund may be forced to go to the bond market and borrow billions of dollars to replenish its statutorily required reserve funding. Now, an influential business group is warning to lawmakers to stay away from tinkering with the fund. “Expanding the size and scope of the Florida Hurricane Catastrophe Fund sends an unfortunate signal to private reinsurance markets that their capital is unwelcome,” reads a special session priorities briefing from Associated Industries of Florida, which represents a range of manufacturers and other businesses. “Policymakers should guard against efforts to adjust its coverages at the expense of depleting its cash build-up,” which could make it more likely that Floridians and business owners could see another surcharge or “hurricane tax.” AIF made similar statements before the 2022 regular legislative session in January. If the Dec. 12 session is anything like the first insurance-dedicated special session, held in May, the reform package will be crafted by legislative leaders and the governor’s office shortly before the session begins. In May, the proposed bills were unveiled less than 48 hours before the Capitol opened, and the bills sailed through in three days with almost no changes. Monday, December 05 2022

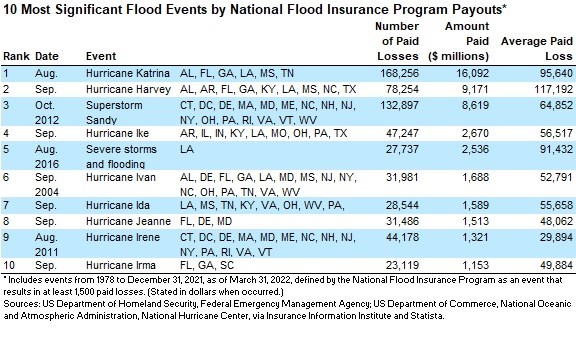

Hurricane Ian may result in one of the largest losses in the history of the National Flood Insurance Program and add to its current $20.5 billion debt. According to a market segment report from AM Best, the projected range of Hurricane Ian losses of between $3.5 billion and $5.3 billion from the Federal Emergency Management Agency would potentially be below the program’s reinsurance attachment. But recent estimates from modeler CoreLogic are much higher – breaching and perhaps blowing through the reinsurance layer. CoreLogic said flood losses from Ian, which made landfall in Florida on Sept. 28, could be between $8 billion and $18 billion. Hurricane Katrina in 2005 caused $16.1 billion in losses to the NFIP, the most ever (see chart). The NFIP had to borrow $17 billion to pay claims related to Katrina and hurricane Rita and Wilma, which also struck in 2005.

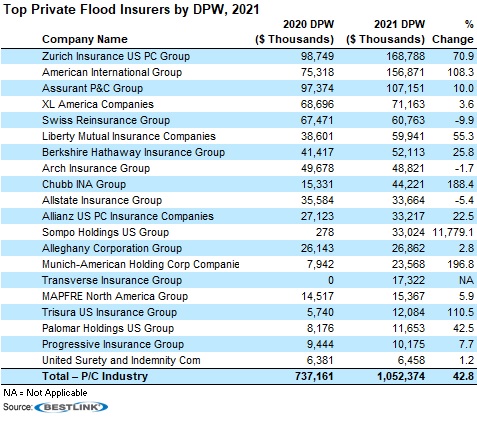

Hurricane Nicole, which also struck Florida after Ian, will result in additional losses. AM Best report titled, NFIP Adrift but Private Flood Insurance Gains Traction, also pointed out that private flood insurers increased direct premiums written by 42% in 2021, the first year Risk Rating 2.0 was implemented to allow for more adequate rates and make private flood insurers more competitive. However, the private flood insurance market remains one-third the size of the federal flood market.

Last year 88% of Florida homeowners with flood insurance saw an increase in NFIP premiums and many will see additional rate increases in 2022 and 2023, “likely driving even more homeowners into the private flood insurance market,” AM Best said. “The full effect of Risk Rating 2.0 has not yet been reached,” the insurance industry rating agency said. “Premium increases are capped at 18% a year on single family primary residences. Based on the limitations on incremental rate increases, the flood premium for many homes will not reach their full actuarially sound rate for another four years.” Thursday, December 01 2022

Florida’s homeowners shell out thousands, even tens of thousands, for property insurance to protect themselves from fierce storms like Hurricane Ian. But tens of thousands of people walloped by the Category 4 storm in September are now discovering that they didn’t have the coverage they needed for one of the biggest impacts of the storm — flood insurance. It’s one of the hardest — and most expensive — lessons from hurricane season 2022, which officially draws to a close Wednesday. Florida’s home insurance market has been troubled for decades, but experts worry that the back-to-back strikes from hurricanes Ian and Nicole could be enough to tilt the teetering market for wind damage insurance into another collapse. Gov. Ron DeSantis has hinted at holding another special session on the topic soon, but it’s not clear if legislators will even try to address the already skyrocketing costs of private insurance and increasing risk load of the state-run option, the Citizens Property Insurance Co. And even if they do, coverage for Florida’s most common risk — flooding — won’t be on the table for discussion. Flood insurance is almost entirely run by the federal government, which sets strict rules and price caps on who needs to have it and how much it costs. Experts say that despite the government’s efforts to make flood insurance cheap and available, Florida faces a massive coverage gap that could grow even larger as the state’s population — and flood risks — grow and the number of policies slowly declines. By one estimate, flood damage could make up half of the total Hurricane Ian losses in Florida. The Category 4 storm tore into Southwest Florida in late September, battering Fort Myers and other areas with two-story storm surge and fierce winds. But it was the slow creep north through the rest of the state, when the much weaker storm dumped more than a foot of rain, that shocked inland residents. Low-lying areas quickly flooded, leaving some apartment complexes with an entire story underwater. Officials had to rescue more than a hundred residents trapped in their homes and cars. The Peace River, in Southwest Florida, swelled from 130 feet wide to nearly a mile wide. And when the floodwaters eventually receded, many Floridians in the path of Ian — and then Nicole — found they weren’t covered for the damages. Only about 18% of homes in Florida counties that were under evacuation orders from Hurricane Ian had a federal flood insurance policy, according to an analysis by risk management firm Milliman. In inland counties, those figures drop even further. Compare Lee County, where Ian made landfall, to Seminole County, north of Orlando. In Lee, about 51% of properties inside flood zones have flood insurance. In Seminole, only 37% do. In either case, that leaves thousands uninsured for flooding damage outside the coverage of most homeowner and windstorm policies. Claims will likely be rejected. “People just expect to be protected and it’s very distressing and upsetting for them to find out they paid the premiums and don’t have the coverage they need,” said Nancy Watkins, a principal and consulting actuary with Milliman. “Often the reason they don’t have a flood insurance policy is they mistakenly think that their homeowner policy would cover that.” Few home insurance policies cover flood damage. Instead, almost all flood insurance policies in the nation are through the FEMA-run National Flood Insurance Program, which insures 1.7 million Floridians. The state actually has the highest number of flood policies under the federal program, but hurricane season 2022 was a sobering reminder of how many people don’t have it. An early estimate by CoreLogic, a property information and analytics firm, suggested that half of the flood damage Florida saw from Ian could be uninsured. Tom Larsen, CoreLogic’s vice president of hazard and risk mitigation, said his firm also found Ian’s damage in Florida extended outside FEMA’s flood zones. “We saw more damage outside those zones than in,” Larsen said. “It doesn’t take much water to cause a lot of damage.”

How much damage did the hurricanes do?Florida’s Office of Insurance Regulation has tallied nearly $10 billion in total losses from Hurricane Ian so far. That includes losses to homes, commercial properties and private flood insurance claims. Initial estimates from FEMA suggest the federal flood insurance program, which insures the vast majority of Floridians with flood policies, could see $3.5 billion to $5.3 billion in losses from all five states hit by Ian, with the majority of those claims coming from Florida. Florida’s relatively small private flood insurance market, with just under 100,000 policies as of late 2021, also took a hit. Trevor Burgess, CEO of Neptune Flood, said his firm has about a third of Florida’s private flood insurance policies. He ranked Ian as the most expensive storm the firm has dealt with since it started five years ago but didn’t offer a dollar figure estimate. “Ian will be our largest claim event after Ida last year,” he said. “Having them year after year is consequential.” For Hurricane Nicole, Florida’s total property losses are slimmer but still significant at just under $400 million. What does flood insurance cover?For the lucky few that had the proper insurance to match their hurricane-borne flood damage, there’s cash from FEMA on the line in at least a few ways. As of mid-November, FEMA said more than 40,000 Floridians have filed Ian-related flood damage claims. They’re likely to get some help patching up their homes, but it likely won’t cover a full replacement. The NFIP, like many of the private flood offerings, is capped at $250,000 of coverage. The picture is worse for those without flood insurance. “An inch of water in your house can easily be a $25,000 expense,” said Watkins. Uninsured people will have to raid their savings or hope for help from charities or state and county grants. Federal grants are not an option. FEMA reserves its grant programs for fixes like home elevation or floodproofing for those with active flood insurance policies. FEMA disaster relief for uninsured properties is usually capped at around $10,000, Watkins said, and it can take a very long time to materialize in people’s bank accounts. Flood insurance numbers droppingYet despite the growing risk of flooding — which Watkins says is the most common disaster facing Floridians — the Sunshine State has fewer and fewer residents with flood insurance every year. Burgess, with Neptune, said his firm produced data showing that 18% of Florida buildings had flood insurance five years ago, and today that figure stands at 15%. “That’s going in the wrong direction. We need many many more people to buy flood insurance to be protected from this peril,” he said. That’s a tough sell in Florida, even considering that sea level rise is making nuisance flooding more common and more intense. The biggest reason is likely that flood insurance, unlike property insurance, isn’t mandatory for most homes. Any home purchased with a mortgage is required to have property insurance, but mortgage-purchased homes are only required to have flood insurance if they’re within a designated FEMA flood zone. And even then, research shows that many of the properties required by their lenders to hold flood insurance policies drop them with no consequences. A recent revamp of the federal flood program, known as Risk Rating 2.0, aims to get more people insured at market rate premiums, a move that could help the NFIP dig itself out of its $20 billion debt hole. For Joel Scata, an attorney with the Natural Resources Defense Council’s water and climate team, the flood damage from Hurricane Ian is another indication that the federal program needs to be reformed to encourage people to live farther away from risky areas. “Floods, in general, are becoming more frequent, both inland and on the coast, because of sea level rise and intense rainstorms,” he said. “The NFIP has the opportunity to be a linchpin in the U.S. approach to mitigating flood risk in regards to climate change.” Average flood insurance premiums are around $600 a year in Florida, according to data collected by Forbes. That makes Florida one of the cheapest states in the nation for flood insurance, despite home and windstorm insurance premiums that are some of the highest in the nation at more than $4,000 a year. “People don’t want to pay more money to buy more coverage that they don’t have now,” Watkins said. “But you don’t find out you need it until it’s too late.” |

Personal Service at Internet Prices!

|

|

|

© Olson & DiNunzio Insurance Agency, Inc., 2008

2536 Northbrooke Plaza Drive; Naples, FL 34119

Doing Business in the State of Florida

P: 239-596-6226; F: 239-596-1620; E: info@olsondinunzio.com

Featuring the cities of Naples, Bonita Springs, Marco Island and Estero Florida. Providing them the highest quality insurance and unbeatable rates.

Insurance Website Design