In recent weeks, pressure has mounted on lawmakers to do something – anything, really – about the rapidly deteriorating home insurance market in Florida. Homeowners across the state are getting policy cancellation notices in droves, forcing them to hunt desperately for any company that will ensure the house where they live. An easy solution to this growing problem, though, remains elusive.

But the first step toward solving a problem, as the saying goes, is to admit you have one.

On that front, Florida leaders, from Gov. Ron DeSantis to Senate President Wilton Simpson and House Speaker Chris Sprowls, have at least acknowledged that Florida has a crisis on its hands. It’s a crisis that has been hard to miss: six property and casualty insurance companies have become insolvent since 2017, and six others have taken drastic steps to reduce their exposure in Florida, with some pulling out of the state completely, others canceling their riskier Florida policies, while the rest have simply refused to take on new Florida customers.

Why are Florida insurers in such dire straights?

Big storms cause big problems

A combination of factors is to blame, starting with the simple and unavoidable fact that Florida is a gigantic peninsula jutting out into the warm, hurricane-friendly waters of the mid-Atlantic Ocean and Gulf of Mexico.

The state has gotten clobbered with its fair share of extremely devastating hurricanes since 2016: Hurricane Hermine trashed the state’s capital city and surrounding communities in 2016, followed almost immediately by Hurricane Matthew. And although Matthew technically missed landfall, it nevertheless brushed violently along the entire length of Florida’s east coast, close enough to cause significant damage to homes and businesses along 250miles of some of Florida’s most expensive beachfront property.

The very next year, Hurricane Irma slammed into the Florida Keys and then took the absolute worst possible path, straight up the center of the state, engulfing vast swaths of residential areas in heavy rains and wind. To this day, it remains the most expensive storm in the history of the state, causing billions of dollars in wind and flood damage, and devastated citrus crops and other industries.

Then, in 2018, Hurricane Michael tried to wipe Mexico Beach off the map. The Category 5 storm tore a path of destruction 100-miles wide by 80-miles long through the heart of the state’s panhandle.

Hurricanes weren’t the extent of the damage, either. There are the tropical storms which bring heavy rain and damaging winds that other states experience far less frequently.

Those damages add up. A billion here, a billion there. Pretty soon we’re talking about real money.

The math doesn’t add up for Florida insurers

On average, insurance companies across the nation pay out an average of $100.70 on every $100 of premiums they take in. While that may sound like a financial loser for the insurance company, they actually make a profit because they invest those premiums before paying them out. Typically, insurance investments make about 7 percent, which is how the companies are able to stay in business and provide homeowners protection from catastrophic damage.

But compared to the rest of the country, Florida is a significant outlier. According to R Street Institute, in 2016-2019, the Florida homeowners insurance market reported a combined ratio of 117.5 percent. This means that for every hundred dollars of premium received, insurers paid $117.50 in losses and expenses. Florida insurers actually outperformed other insurers on the investment side, making about 9 percent, but that still means they ended up losing almost 9 percent overall for every homeowner they insured.

Soaring premiums haven’t kept pace with insurance company losses, and homeowners simply can’t afford much more. No wonder insurance companies are saying they’ve had enough of doing business in the Sunshine State.

The Citizens Insurance: a ticking time bomb

With so many insurers packing up and leaving customers in the lurch, homeowners are increasingly turning to the state’s so-called insurer of last resort: Citizens Insurance, which is subsidized by the state. In late March, Citizens President and CEO Barry Gilway reported that his company would likely have more than one million policies by the end of 2022, and Citizens is adding policies at a clip of 5,500 per week.

A single storm similar to Irma, that takes out a broad swath of residential areas, could cause a financial catastrophe for Florida. In order to manage that much exposure, Citizens is considering a massive 11 percent hike in premiums, but property owners in some areas of the state, like South Florida, would likely pay substantially higher rates than elsewhere.

The rate hikes could lead to their own financial problems for homeowners who simply can’t afford to pay their mortgage and a significant increase in insurance costs. With rising interest rates, Florida’s home market could cool off quick.

Litigation exacerbates the problem

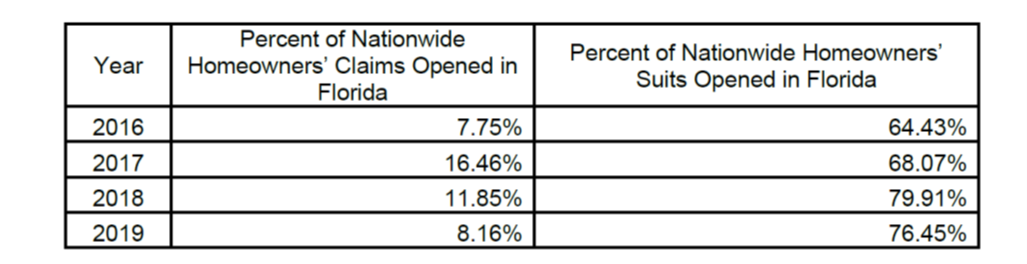

With so many storms, a high number of insurance claims are bound to be filed. And inevitably, more claims means more litigation. But Florida remains an outlier there, too. According to National Association of Insurance Commissioners (NAIC) data mined by the Florida Office of Insurance Regulation, while Florida homeowners insurance claims accounted for just over 8% of all homeowners claims opened by U.S. insurers in 2019, homeowners insurance lawsuits in Florida accounted for more than 76% of all litigation against insurers nationwide.

Simply put, that’s insane, and it’s unsustainable. Something’s got to give.

Fraud and abuse

From sinkholes fears to fake roof damage, to allegedly leaky pipes, there seems to be no shortage of ways bad actors can take advantage of the insurance system to make false or exaggerated claims to bilk policies and drive up costs for insurers and homeowners alike.

Nationally, experts estimate that more than $80 billion in fraudulent insurance payments are made annually. Given Florida’s outsized role in the insurance market, there’s little doubt that a good chunk of that number can be traced back here.

Among the most common fraud schemes: claims for wind damaged roofs after a hurricane, when only normal wear and tear is present. Last month, Florida CFO Jimmy Patronis announced the arrest of two men who were charged with nine counts of fraud in connection with this type of scheme.

Lawmakers have attempted to address the fraud issue in recent years but more can still be done.

Bottom Line

Lawmakers will need to consider a broad range of actions that seek to reduce litigation, cut costs, install stiffer penalties for fraudulent claims, bolster the resources for fraud investigation claims, and revamp Citizens Insurance so that Florida taxpayers are not on the hook after the next major storm.

{kind=link}