BlogWednesday, April 20 2022

In recent weeks, pressure has mounted on lawmakers to do something – anything, really – about the rapidly deteriorating home insurance market in Florida. Homeowners across the state are getting policy cancellation notices in droves, forcing them to hunt desperately for any company that will ensure the house where they live. An easy solution to this growing problem, though, remains elusive. But the first step toward solving a problem, as the saying goes, is to admit you have one. On that front, Florida leaders, from Gov. Ron DeSantis to Senate President Wilton Simpson and House Speaker Chris Sprowls, have at least acknowledged that Florida has a crisis on its hands. It’s a crisis that has been hard to miss: six property and casualty insurance companies have become insolvent since 2017, and six others have taken drastic steps to reduce their exposure in Florida, with some pulling out of the state completely, others canceling their riskier Florida policies, while the rest have simply refused to take on new Florida customers. Why are Florida insurers in such dire straights? Big storms cause big problems A combination of factors is to blame, starting with the simple and unavoidable fact that Florida is a gigantic peninsula jutting out into the warm, hurricane-friendly waters of the mid-Atlantic Ocean and Gulf of Mexico. The state has gotten clobbered with its fair share of extremely devastating hurricanes since 2016: Hurricane Hermine trashed the state’s capital city and surrounding communities in 2016, followed almost immediately by Hurricane Matthew. And although Matthew technically missed landfall, it nevertheless brushed violently along the entire length of Florida’s east coast, close enough to cause significant damage to homes and businesses along 250miles of some of Florida’s most expensive beachfront property. The very next year, Hurricane Irma slammed into the Florida Keys and then took the absolute worst possible path, straight up the center of the state, engulfing vast swaths of residential areas in heavy rains and wind. To this day, it remains the most expensive storm in the history of the state, causing billions of dollars in wind and flood damage, and devastated citrus crops and other industries. Then, in 2018, Hurricane Michael tried to wipe Mexico Beach off the map. The Category 5 storm tore a path of destruction 100-miles wide by 80-miles long through the heart of the state’s panhandle. Hurricanes weren’t the extent of the damage, either. There are the tropical storms which bring heavy rain and damaging winds that other states experience far less frequently. Those damages add up. A billion here, a billion there. Pretty soon we’re talking about real money. The math doesn’t add up for Florida insurers On average, insurance companies across the nation pay out an average of $100.70 on every $100 of premiums they take in. While that may sound like a financial loser for the insurance company, they actually make a profit because they invest those premiums before paying them out. Typically, insurance investments make about 7 percent, which is how the companies are able to stay in business and provide homeowners protection from catastrophic damage. But compared to the rest of the country, Florida is a significant outlier. According to R Street Institute, in 2016-2019, the Florida homeowners insurance market reported a combined ratio of 117.5 percent. This means that for every hundred dollars of premium received, insurers paid $117.50 in losses and expenses. Florida insurers actually outperformed other insurers on the investment side, making about 9 percent, but that still means they ended up losing almost 9 percent overall for every homeowner they insured. Soaring premiums haven’t kept pace with insurance company losses, and homeowners simply can’t afford much more. No wonder insurance companies are saying they’ve had enough of doing business in the Sunshine State. The Citizens Insurance: a ticking time bomb With so many insurers packing up and leaving customers in the lurch, homeowners are increasingly turning to the state’s so-called insurer of last resort: Citizens Insurance, which is subsidized by the state. In late March, Citizens President and CEO Barry Gilway reported that his company would likely have more than one million policies by the end of 2022, and Citizens is adding policies at a clip of 5,500 per week. A single storm similar to Irma, that takes out a broad swath of residential areas, could cause a financial catastrophe for Florida. In order to manage that much exposure, Citizens is considering a massive 11 percent hike in premiums, but property owners in some areas of the state, like South Florida, would likely pay substantially higher rates than elsewhere. The rate hikes could lead to their own financial problems for homeowners who simply can’t afford to pay their mortgage and a significant increase in insurance costs. With rising interest rates, Florida’s home market could cool off quick. Litigation exacerbates the problem With so many storms, a high number of insurance claims are bound to be filed. And inevitably, more claims means more litigation. But Florida remains an outlier there, too. According to National Association of Insurance Commissioners (NAIC) data mined by the Florida Office of Insurance Regulation, while Florida homeowners insurance claims accounted for just over 8% of all homeowners claims opened by U.S. insurers in 2019, homeowners insurance lawsuits in Florida accounted for more than 76% of all litigation against insurers nationwide. Simply put, that’s insane, and it’s unsustainable. Something’s got to give. Fraud and abuse From sinkholes fears to fake roof damage, to allegedly leaky pipes, there seems to be no shortage of ways bad actors can take advantage of the insurance system to make false or exaggerated claims to bilk policies and drive up costs for insurers and homeowners alike. Nationally, experts estimate that more than $80 billion in fraudulent insurance payments are made annually. Given Florida’s outsized role in the insurance market, there’s little doubt that a good chunk of that number can be traced back here. Among the most common fraud schemes: claims for wind damaged roofs after a hurricane, when only normal wear and tear is present. Last month, Florida CFO Jimmy Patronis announced the arrest of two men who were charged with nine counts of fraud in connection with this type of scheme. Lawmakers have attempted to address the fraud issue in recent years but more can still be done. Bottom Line Lawmakers will need to consider a broad range of actions that seek to reduce litigation, cut costs, install stiffer penalties for fraudulent claims, bolster the resources for fraud investigation claims, and revamp Citizens Insurance so that Florida taxpayers are not on the hook after the next major storm. Tuesday, April 19 2022

Florida Gov. Ron DeSantis said Monday that he will call a special session of the legislature to address rising property insurance rates in the state. The Republican governor said the special legislative session will occur in May and focus mainly on the “reform of the property insurance market" but could address other topics. He said he would sign a proclamation this week containing meeting dates and additional details. DeSantis said the goal on property insurance would be to “bring some sanity and stabilize and have a functioning market.” The announcement comes amid growing consensus among lawmakers to address spiking rates and other problems in the state's property insurance market. Attempts to pass legislation around property insurance failed during the regular legislative session in the GOP-controlled statehouse earlier this year. “After months of public outcry, newspaper headlines, and Democrats raising the alarm all session long, the Governor has finally addressed the growing homeowner’s insurance crisis," said Sen. Jeff Brandes, a Republican who has been pushing for a special session on property insurance. Joseph Petrelli, president of Demotech, a company that rates the financial stability of insurers, said one prime factor driving up Florida’s homeowner rates is state court rulings that have made it highly profitable for lawyers to sue insurance companies even if the amount won is relatively small. Petrelli added that Florida's premiums are also driven up by its rules governing roof replacement, with the state requiring that any roof incurring damage of 25% or more in a storm or other event must be fully replaced. But Amy Boggs, a St. Petersburg attorney who chairs the Florida Justice Association's property insurance committee, disputed Petrelli's contentions. She said one problem is that the insurance companies are claiming they aren't profitable, but their financial records are not made public so it is impossible to test the veracity of their claims. She said the Legislature passed a law last year limiting attorney fees, so that is no longer an issue. For roofs, she said, if insurance companies are not going to have to fully cover older roofs, they should be required to tell consumers how much they are covering and how much that will decrease the premium. She said the only reason the number of lawsuits in Florida is high is that insurance companies often try to stiff their customers out of tens of thousands of dollars. She said in one recent case she handled involving a home destroyed in Hurricane Irma, the property insurer tried to pay about $2,000, saying the damage was caused by flooding that its policy didn't cover. She said arbitrators disagreed and ordered the company to pay $233,000. “No one is suing over a couple thousand dollars,” Boggs said. Monday, April 11 2022

If the Florida homeowners’ insurance market were in a medical exam, the diagnosis would find the patient in dangerously poor condition. The patient’s vital signs—its financial results—are troubling. What is more, there are multiple co-morbidities. The welter of symptoms collectively reveal the patient to be one step away from the emergency room. Consider seven signs of sickness below: 1. Red Ink. Insurers operating in Florida overwhelmingly report unprofitable results. Insurance companies collectively lost $1.5 billion of their Florida business in 2021, a year in which no hurricanes struck the peninsula. In 2016-2019, the Florida homeowners insurance market reported a combined ratio of 117.5 percent. This means that for every hundred dollars of premium received, insurers paid $117.50 in losses and expenses. This compares to the overall insurance industry reporting a combined ratio of 100.7 percent. The industry’s investment income ratio—investment income divided by net premium—of 7.9 percent renders the results of the overall industry profitable, with a seven-point profit margin. The investment income is not, however, sufficient to pull Florida homeowners business into the black, as figuring in investment income resulted in an operating margin of 109.6 percent, which means Florida homeowners insurers on average lose $9.60 for every hundred dollars of premium revenue. 2. Administration of Last Rites. Several Florida insurers have become insolvent in recent months and years. The common denominator in these companies’ corporate obituaries is claims costs far outpacing premium growth. The most recent casualties include Gulfstream, Avatar and Johns.

3. Be a quitter. Several property insurers are realizing that continuing in the Florida market is throwing good money after bad, and are strategically withdrawing from the state. The most recent such announcement, in March, was from Lexington Insurance Company, part of the American International Group family. What makes Lexington’s departure troubling is that Lexington is an excess and surplus (E&S) lines insurer. E&S companies concentrate on high-risk business no standard insurer will touch. Whereas standard insurers run out of burning buildings (figuratively), E&S carriers run into burning buildings. Because they are willing to insure business others won’t, regulators allow E&S insurers the freedom to charge premiums and issue insurance contracts as they see fit, without having to abide by the guardrails established by state-based insurance regulators overseeing standard lines insurer rates and forms. 4. Limit your losses. Insurers continuing to operate in the Sunshine State are taking defensive tactical measures, cancelling policies, restricting coverage and raising rates (see table below).

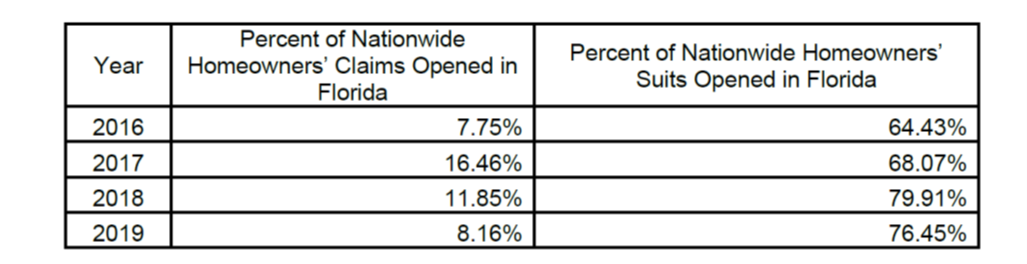

5. Those who fight and run away live to fight another day. The growth and profitability strategy for insurers with a Florida footprint is to increase their business outside of the state while shrinking their Florida portfolio. For example, Heritage insurance, 86 percent of whose 2021 business was in Florida, reported in its Q4 2021 earnings call that it had a 10.9 percent decrease in Florida personal lines policies and a 10.7 percent increase in personal lines outside of Florida. 6. The Swelling of Citizens. Citizens Property Insurance Company (Citizens), the state-run “insurer of last resort” is becoming the “insurer of first resort” as private market insurers refrain from offering coverage to customers who cannot find insurance elsewhere. In late March, Citizens President and CEO Barry Gilway projected his company could have more than one million policies by the end of 2022. Citizens is adding approximately 5,500 new policies per week. At the end of March 2022, Citizens had 801,341 policies, up from 570,000 one year ago. 7. Litigation Gone Wild. In a recent Citizens report, Gilway also noted a “disturbing trend” in year-to-date litigation through June of 2021—the number of lawsuits against insurers, excluding Citizens, increased 51 percent year-over-year to 50,951 versus 33,800 in the first six months of 2020. The longer-term picture is disturbing—the same report reveals that the rise in Florida homeowners’-related lawsuits more than tripled from 27,416 in 2013 to 85,007 in 2020. Litigation, Litigation, Litigation Unlike several Louisiana insurers that succumbed to losses from Hurricane Ida in 2021, Florida insurance failures and pullouts were not driven by natural catastrophe losses. The cause of the Florida woes is excessive litigation. Although excessive litigation is the proximate cause of Florida’s property insurance issues, it’s not appropriate to blame the lawyers. Lawyers litigate—that’s their job. The problem has arisen from the unintended consequences of a cluster of laws and state Supreme Court decisions that created loopholes enabling contractors, lawyers and homeowners to inflate the number and the value of claims payments. A comprehensive report by Guy Fraker on the dire condition of the Florida insurance concurs with this assessment, finding that “everybody’s just leveraging the rules of the game.” The Florida Office of Insurance Regulation 2020 annual report presents the striking statistic that “in 2019 Florida accounted for 76.45% of all homeowners’ suits opened against insurance companies in the U.S. despite only accounting for 8.16% of all homeowners’ claims opened by insurance companies in the U.S.” The Cure Reform of the broken Florida homeowners insurance market requires resolve in the state legislature to pass a sweeping set of reforms. In the legislative session ending March 2022, the only significant bill to be presented was SB 1728, which was temporarily postponed, and ultimately failed due to never being reconsidered in the final days of the 60-day regular session. This bill takes aim at unscrupulous roof contractors, but it is medicine too thin for a patient seriously ill that may go on life support if this year’s hurricane season is rough. Just as operating on a patient suffering from multiple diseases is complex, solving the Florida insurance issues is no easy undertaking. We suggest the following legislative initiatives be introduced:

SB 76, approved in the 2021 legislative session, took aim at unscrupulous roofing contractor solicitation practices, including contractors making promises for “free roofs” when any damage is the result of roof age rather than wind damage. A federal court blocked that portion of the bill, alleging that roof contractor solicitations are a form of protected free commercial speech. SB 1728, as introduced in the 2022 legislative session, would allow contractor solicitation and advertising provided the contractor present a statement to the homeowner clarifying that the homeowner is responsible for paying the deductible. The statement also stipulates that it is a felony for the contractor to waive the deductible or file a claim with false information. It would also introduce a roof-only deductible for new policies.

Without a special session focusing on addressing the pressing Florida property insurance problems, it appears likely that the situation will only get worse. June 1 is the date for renewal of reinsurance treaties protecting Florida insurers. Expectations are for reinsurance rate increases, which will be passed on to homeowners, pushing Florida homeowners insurance premium levels to yet higher nosebleed levels. June 1 is also the official start of the Atlantic hurricane season. If there is a silver lining to this cloud, it is that additional pain may spur legislators to take action and support needed reforms, and to do so with dispatch. Thursday, March 31 2022

In yet another ominous sign for Florida’s failing property insurance market, Tampa-based Lighthouse Property Insurance Corp. lost its financial stability rating, which means it will likely be placed under state receivership and dissolved. On Wednesday, ratings firm Demotech announced the withdrawal, effective Tuesday, of Lighthouse’s former A rating. “Despite a substantial capital contribution in the fourth quarter 2021, the operating loss in 2021, which reflected the evaluation of losses and loss adjustment expenses associated with Hurricane Ida, resulted in a level of capitalization below what was needed to sustain [its stability rating] at the A level,” Demotech president Joseph Petrelli said in a brief news release. Lighthouse reported having 13,200 policies in Florida at the end of 2021. Of those, 947 were in Broward, Palm Beach and Miami-Dade counties. Those policyholders will have to find new carriers or go into state-owned Citizens Property Insurance Corp. if the state Office of Insurance Regulation seeks a court order to put Lighthouse in receivership. Hurricane Ida, the fifth-costliest hurricane on record, struck the Gulf Coast on its way toward the Northeastern United States. Lighthouse also wrote policies in Louisiana, North Carolina, South Carolina and Texas. Demotech, in a letter signed last week by Petrelli and the company’s other top executives, warned Gov. Ron DeSantis, Senate President Wilton Simpson and House Speaker Chris Sprowls that failure to call a special session to address financial instability of the state’s insurance market would likely force Demotech to withdraw financial stability ratings of “a number” of companies. Demotech withdrew Lighthouse’s stability rating just hours after DeSantis called a special session to address congressional redistricting but not the insurance crisis. DeSantis later told reporters that he expected property insurance reform to be dealt with by the legislature “sometime this year” and possibly not until after the 2022 election in November. That’s when Sprowls, who refused to take up several reform bills considered in the Senate, will be replaced as House speaker. Loss of Lighthouse’s rating follows failure of four Florida-based property insurers since April 2021. In February, state officials announced that Orlando-based St. Johns Insurance, a former top-10 insurer with more than 200,000 policies as recently as 2019, went into receivership after losing its financial stability rating. Slide, a newly formed insurer, agreed to absorb 147,000 of the St. Johns policies, preventing those homeowners from having to find new carriers willing to take them. Earlier this month, about 37,000 customers of Avatar Property & Casualty weren’t so fortunate. They were given until April 13 to find new insurers after that company lost its rating. A spokeswoman for the Florida Office of Insurance Regulation, which typically oversees initial steps in insurance company liquidations, did not immediately respond to a request for comment about the Lighthouse rating withdrawal. But when an insurer loses its financial stability rating, “it’s highly likely that the state will put it into receivership,” said Paul Handerhan, president of the consumer-oriented watchdog group Florida Association for Insurance Reform. Federally-backed mortgage guarantors such as Freddie Mac and Fannie Mae will not approve mortgage loans if properties are insured by carriers without Demotech’s A rating. Together, about 50 Florida-based insurers reported more than $1 billion in operating losses in 2021. Insurers say the industry is being torn apart financially by severe weather claims, roof replacement claims, contractor fraud, and excessive litigation. State records show that Lighthouse was sued 116 times in 2020 and 269 times in 2021. Since Jan. 1, 41 suits have been filed against the company. More than 100,000 lawsuits were filed against Florida insurers last year. Florida accounts for 76% of all property insurance litigation in the country, state insurance regulators said last year. Tuesday, March 29 2022

Florida’s home insurance availability crisis continues to claim new victims, and worries are mounting that more companies could be declared insolvent as this year’s hurricane season draws near. The industry’s financial storm clouds have prompted fears of collapsing companies and the massive growth of state-owned Citizens Property Insurance Corp., the insurer of last resort:

Last week, Gov. Ron DeSantis said he’d “welcome” a special session to enact insurance reforms, but indicated he would not call one on his own. Instead, he left the proposal up to leaders of the state Senate and House. So far, there’s been no indication that Senate President Wilton Simpson and House Speaker Chris Sprowls plans to call a special session, said Sen. Jeff Brandes, a Tampa-area Republican who has repeatedly warned that the state faces an insurance crisis that could undermine Florida’s booming real estate market. The Senate passed a bill in the recently completed regular session aimed at curbing the number of “free roof” claims and related lawsuits that insurers say are driving up costs for all of their customers. But the House refused to consider any major insurance reforms. The foreboding letterIn Demotech’s March 23 letter to DeSantis, Simpson and Sprowls, five Demotech executives, including its president and co-founder Joesph Petrelli, warned that failure to enact reforms before the June 1 start of hurricane season would lead to grave consequences. “The conditions of the property insurance marketplace in Florida are unsustainable,” the letter said, “and without the necessary corrective action, many Florida insurers will struggle to maintain adequate surplus, efficient capital sources will avoid the market, private reinsurance costs will become prohibitively expensive, and consumers will ultimately bear the cost.” Longtime leaders in the insurance industry believe that some companies won’t have enough cash, financing, or investment capital to purchase reinsurance, which is required so insurance companies have the ability to cover claims likely to roll in after a 1-in-100-year storm event, such as a major hurricane. Insurers that fail to maintain an adequate surplus of claims-paying capital could be declared insolvent by state insurance regulators, and their policyholders would likely be forced into Citizens. Citizens’ growth always prompts worries: If it grows too much and cannot pay all claims after a major hurricane, assessments could be levied against nearly all insurance policies in the state to make up the shortfall. Citizens, which was down to 419,000 policies in 2019, has been quickly swelling with new customers who can’t get covered in the private market. As of March 25, Citizens was up to 807,910 policies. Four Florida-based insurers have been declared insolvent since April 2021. Many others have stopped writing policies in high-claims areas of the state, such as South Florida, and declined to renew policies covering older homes or homes with roofs older than 10 years. Insolvencies could also result from Demotech withdrawing companies’ financial strength ratings or downgrading companies’ ratings from A for “acceptable” to S for “satisfactory.” A downgrade effectively puts a company out of business, either by prompting state insurance regulators to declare the company insolvent and transfer it to a receiver, or, in the case of any rating lower than A, disqualifying the insurer from covering any property backed by a federal mortgage guarantor, such as Fannie Mae and Freddie Mac. Demotech’s letter warned lawmakers to expect ratings downgrades if no special session is called. “If current market conditions remain in place, we anticipate that we will downgrade Financial Strength Ratings of a number of companies in the coming weeks,” the letter said. Simpson has called the idea of a special session to address insurance “a possibility,” according to a March 11 statement relayed by a spokeswoman. Sprowls’ office on Monday did not respond to questions about a special session. More companies might have to fail before the Senate and House leaders call a special session, Brandes said. “Sometimes you have to force a crisis to get the legislature to act,” he said. Replacement policies hard to find with open claimsA former Avatar policyholder says she’s already facing a crisis. Mimi Bright, a homeowner in Parkland, has been trying to find coverage since learning her Avatar policy would expire in mid-April. But she has an open damage claim with Avatar, and her agent told her that no insurer, including Citizens, will cover her until the claim is resolved. That could take several months. Under terms of Avatar’s liquidation, the company’s open claims will be resolved by the Florida Insurance Guaranty Association, which is working its way through about 2,000 open Avatar claims. She doesn’t understand why state law does not require Citizens to offer coverage to policyholders left in limbo when their insurers are declared insolvent. “The state should be doing something to protect consumers,” she said. Despite what its underwriting guidelines say, Citizens is willing to cover Bright and other Avatar customers with open claims if they provide documentation that the claim has been submitted and repairs are in progress, says Citizens spokesman Michael Peltier and Kyle Ulrich, president and CEO of the Florida Association of Insurance Agents. “Obviously, [the Avatar dissolution] happened quickly, and we will be as flexible as we can be,” Peltier said. Homeowners will have to provide proof, such as a repair contract showing that repairs have been scheduled or proof that the repair process is underway, he said. Agents have to be tenacious and offer to provide the documentation, which could also include price estimates from contractors, Ulrich said. Citizens, Ulrich says, understands that “It’s in no one’s interest to have homeowners go without coverage for a period of time.” Corey Neal, executive director of the Florida Insurance Guaranty Association, said FIGA is willing to work with agents to provide information needed to help displaced homeowners secure replacement coverage. Some private-market companies, and not just Citizens, will cover a stranded homeowner when FIGA or a policyholder’s agent reaches out, Neal said. “If the underwriter wants more information about a loss, we’ll absolutely help them. One of our first priorities is to help find replacement coverage. Hardship claims go to the top of the list.” The key, he said, is for agents not to accept “no” for an answer from a company’s underwriting staff and to appeal to a higher level, such as an underwriting department manager. Agents needing help can reach out to FIGA directly, he said. Information about the Avatar liquidation can be found at avatar-liquidation.com. Paul Handerhan, president of the consumer focused watchdog group, Federal Association for Insurance Reform, said consumers whose insurers decline to renew them also face difficulties finding replacement coverage if they have open claims. “It’s becoming a real problem, especially with the growing number of non-renewals,” he said. Progressive Insurance recently announced plans not to renew 56,000 Florida homes with roofs older than 15 years. FAIR would like to see a state law requiring Citizens to cover displaced policyholders with open claims. The law could allow Citizens to exclude the damaged section of those homes from coverage until repairs are complete. Lexington pullout to affect wealthyLexington Insurance Co.’s decision to stop insuring private homes as of Aug. 1 could be a signal that costly claims are also affecting viability of the so-called surplus lines market that typically caters to wealthier clients with homes worth $1 million or more. Most of Lexington’s policyholders don’t have the option to get coverage from Citizens because Citizens only insures homes with replacement values of $700,000 or less in all counties except Miami-Dade and Monroe, which caps eligible replacement values at $1 million. Lexington told agents last week that it plans to terminate its personal lines coverage program as of Aug. 1. Lexington’s parent company, AIG, declined to comment on the decision. Handerhan said he was told that Lexington is pulling out of the homeowner market across the country. Lexington insures 8,000 homes in the state with replacement values totaling more than $90 million, Handerhan said. Ryan Papy, president of the Palmetto Bay-based Keyes Insurance agency said Lexington’s decision could prove costly to the growing number of Florida homes valued at $1 million or more. Lexington customers who must look elsewhere will find “that market is almost empty,” Papy said, adding other surplus lines carriers, such as Chubb and Pure “have no appetite for new business.” Cost increases “could be substantial — 100% to 200% even,” he said. “Maybe more.” “The market turmoil is going to begin to affect a different type of customer,” he said of the wealthier homeowners. “That may push things closer to reform.” Thursday, March 17 2022

Two men are facing charges for an alleged roofing scheme that targeted homeowners’ insurance companies across Southwest Florida following Hurricane Irma, officials said. Brian Webb and Brandon Jourdan, 41, of Cape Coral are accused of convincing homeowners in Lee and Collier counties to submit claims to their home insurance companies with promises of a rebate that would cover their deductible, according to Florida’s Chief Financial Officer Jimmy Patronis. The two operated Webb Roofing & Construction LLC, court records show. As part of the scheme, the pair allegedly enticed homeowners to submit a full roof replacement claim to their insurance related to damage allegedly caused by Hurricane Irma. Webb and Jourdan are accused of telling their sales team to ‘solicit insured homeowners with a promise they can get them a new roof without paying the required homeowner’s deductible,’ Patronis reported. The sales team was reportedly told to convince homeowners to submit claims for “damaged” roofs related to Hurricane Irma for full roof replacements. As part of the con, employees had homeowners sign over their insurance claim rights and have them sign an ‘advertising agreement’ where they agreed to have signs placed in their yard, post positive reviews, and give referrals in exchange for the rebate or a credt towards the deductible amount. Webb and Jourdan are facing nine felony counts of false & fraudulent insurance claims. They could each face a maximum sentence of up to a $45,000 fine and up to 45 years in prison. Webb was booked into the Collier County Jail Tuesday. Jourdan was booked into the Lee County Jail on March 12 and released on bond a day later. A judge set Webb’s bond at $45,000. Tuesday, March 15 2022

Florida homeowners will probably have to continue riding out a turbulent property insurance market on their own for the next year after state lawmakers ended their annual legislative session without enacting any reforms. House and Senate leaders couldn’t agree during the roughly 60-day session on a solution to relieve homeowners of double-digit rate increases, so they passed nothing. “Bottom line: Homeowners lost, and that’s what troubles me,” said Sen. Jim Boyd, R-Sarasota, who sponsored the main property insurance reform bill in the Senate. Short of calling lawmakers back to Tallahassee for a special legislative session to address the problem — which some senators said was a possibility — homeowners can expect no new relief to their bills in 2022. The property insurance industry is widely believed to be in crisis. Homeowners’ rates have been going up by double digits the last few years, and more than a dozen companies have recently suspended new business in Florida, limited the types of homes they cover or canceled policies outright. A handful of companies have gone out of business in the last two years. Multiple lawmakers said this year that rising property insurance rates were one of the most common complaints they were hearing from constituents. When asked Monday about the Legislature’s failure to pass a property insurance bill, Gov. Ron DeSantis pivoted to discuss the rising costs of inflation, which he has frequently blamed on President Joe Biden and Congress. “I supported a lot of the stuff the Senate was talking about on a variety of these things,” said DeSantis, who is running for reelection this year. “I stand ready to do even more, but people should just be prepared: The gas, the groceries, utilities, all these things are going to go up in an era of fighting inflation.”

LOOKING TO ROOFS FOR A POSSIBLE SOLUTION One issue lawmakers had hoped to tackle was the high number of roof replacement claims that industry executives say are partly to blame for rising prices. Many companies say they are now refusing to insure homes with older roofs as a result of the number of fraudulent roofers who are going door to door convincing homeowners that they can file a claim to have their roof replaced. Last year, lawmakers tried to limit the types of advertisements roofers could offer, but a federal judge temporarily blocked it. This year, Boyd’s Senate Bill 1728 would have required roofers to inform homeowners that they’re responsible for paying any deductibles and alert them that it’s illegal for a contractor to pay or rebate the cost of the deductible. It also originally would have allowed insurers to offer policies that would only pay the depreciated value of the roof, or an “actual cash value” — an idea that would almost certainly leave Floridians with older homes footing most of the bill. That idea was dropped in lieu of requiring homeowners to pay a 2% deductible for roof replacements, something considered more palatable to lawmakers. For a $400,000 home, for example, the homeowner would have had to pay a deductible of up to $8,000, or 2%, to replace a roof, with the insurer picking up the rest. The deductible would not have applied if the home was a total loss or if the roof was destroyed by a hurricane. Replacing a shingle-roofed home can cost anywhere from about $9,000 to more than $25,000 depending on the size of the home and shape of the roof. “It wouldn’t fix the problem, but we thought it would help the problem,” said Boyd, who is an insurance broker. The Senate passed the bill, but House leadership wouldn’t accept it. On Thursday and Friday, with time running out for the legislative session, negotiations hinged on the House’s insistence on modifying the deductible plan. They wanted it to be optional for insurers, not mandatory. It’s already optional for insurers, though, Boyd said. “It just wouldn’t have made any difference to the problem.” House Speaker Chris Sprowls, R-Palm Harbor, said he had serious questions about the Senate’s 2% deductible plan, including whether it would make any difference to homeowners’ rates. He raised a scenario of wind causing a tree to fall and destroy a homeowner’s roof. “Does that mean you’ve got to pay 2% of your deductible, and really, it’s just sort of an act of God?” Sprowls said Monday. “I think that there’s a lot of issues like that.” LITIGATION IS AN ISSUE Sprowls also noted that lawmakers passed a property insurance bill last year, and that insurers say it takes 18 months for such reforms to make much effect. “It’s frustrating for me as a homeowner. It’s frustrating for a lot of people,” Sprowls said of skyrocketing rates. “But I want to make sure that we’re making the right reforms that are going to have an impact on the marketplace and don’t inadvertently have an adverse impact on homeowners.” There are several reasons why some insurers are struggling. According to a 2019 Florida Office of Insurance Regulation study, the state made up 8.16% of all homeowners’ claims in the country, but 76.45% of the nation’s lawsuits. The cost of reinsurance, which insurers buy to cover their claims, has gone up. And some companies that have gone out of business appear to have struggled for everyday business reasons. The industry’s woes are affecting consumers directly. After Orlando-based St. Johns Insurance went into receivership last month, the Florida Insurance Guaranty Association approved adding a 1.3% increased assessment on all policies sold in the state. To Joe Petrelli, CEO of Demotech, which rates Florida insurers, the proposed legislation didn’t go far enough to deal with the amount of litigation in the industry. “Absent meaningful and significant tort reform, everything else is a drop in a bucket and a Band-Aid,” Petrelli said. Without that reform, Petrelli said he didn’t see things improving for consumers any time soon. “I think it’s going to be disastrous all the way around, for consumers, insurance companies, modeling companies, rating agencies, and, of course, regulators.” Senate President Wilton Simpson, R-Trilby, said there is a “possibility” that lawmakers will return for a special legislative session. The last time the Legislature went into a special session over property insurance was 2007. “We were disappointed we couldn’t get more done this year, but that’s part of the process,” Simpson said last week. “And so we decided it would be better for the next Legislature to take that issue up.” Wednesday, March 09 2022

St. Johns Policy Holders Due to hurricane losses, fraudulent roof claims and excessive claims litigation St. Johns Insurance Company is now insolvent and will be liquidated by the Florida Department of Insurance. Under the liquidation order starting on March1 2022, all of St. Johns Florida insurance policies are going to be cancelled and immediately transitioned to Slide Insurance Company. Your Slide coverage will begin immediately and it will continue to provide the same coverage as your prior St Johns policy for the remainder of your current policy term. There will be no gaps or changes in the terms of your new Slide policy. Your coverage and the premium will be exactly the same as your old St. Johns policy. When your replacement policy expires, you will receive an offer for a twelve month Slide policy. This renewal policy may have different terms of coverage and different premiums than the replacement policy. Slide will notify your mortgage company, if you have one, and provide all required information. Slide will send your invoice to your mortgage company for payment. How to Make a Payment Call Slide Customer Service at (800) 748-2030. Mail Payment to: Overnight payment: Slide Slide How to File a Claim Claims incurred prior to March 1, 2022: Call: (877) 748-2059 or Customer Service: (800) 748-2030

Call Slide Insurance claims at (866) 230-3758 or Slide Insurance Customer Service at (800) 748-2030 or https://slideinsurance.com/stjohns/ Wednesday, March 02 2022

Citizens plays a unique role in Florida’s property insurance market by providing coverage to eligible policyholders who can’t find it at comparable rates in the private market. One reason Citizens is often the least expensive option is the way we’re built. Unlike a private insurance company, Citizens is required by law to levy assessments on its customers if funds set aside to pay claims have been exhausted after a major storm or series of less severe storms. For Citizens policyholders, those assessments can be substantial. While Citizens remains in a strong financial position, it’s important that you understand the assessment process and how it impacts you. Here’s how assessments work:

That can add up. For a single policy with a $3,000 premium, Citizens’ Policyholder Surcharge alone could mean an additional $1,350 charge when you may already be recovering from a catastrophic loss. Don’t panic! Citizens purchases reinsurance and sell bonds to protect its $6.5 billion surplus and reduce the chance that its customers will be hit by a “hurricane tax” when they are least able to afford it. Since 2015, Citizens has had sufficient claims paying ability to handle a 1-in-100-year storm without having to seek assessments. But the risk of assessment is real, especially as Citizens continues to see its policy count rise in the face of challenges in the private market. Citizens’ customers can reduce their assessment risk by finding coverage with another company. Talk to your agent, who is in the best position to help you find the option that best fits your needs. Monday, February 28 2022

Things are moving fast in Florida’s distressed property insurance market. Just days after St. Johns Insurance Co. announced it would stop writing new homeowner business in Florida, the Demotech rating agency withdrew the carrier’s financial stability rating on Thursday, due to the company’s lack of sufficient reserves and bleak financial reports. A day later, the Tampa-based insurtech startup known as Slide agreed to take over St. Johns’ homeowners book of business, Demotech and other sources have confirmed. "We talked with Bruce Lucas and his company and we’ll probably assign a rating in the near future,” said Demotech President Joe Petrelli. Lucas is CEO of Slide, a startup that has gained considerable attention after the company announced it had raised $100 million in capital last November. Lucas also is known for his success with Heritage Insurance, which grew rapidly into a super-regional insurer serving 15 states. Company officials could not be reached for comment Friday. Also this week, Avatar Property & Casualty Insurance, based in Tampa, announced that it, too, had stopped writing new business in the state as of Thursday, making it the seventh company in recent weeks to suspend new writing or to non-renew thousands of policies in Florida. “After careful consideration, we are taking precautions for the best interests of our policyholders, agents, business partners, and associates,” Avatar said in a bulletin to agents. Demotech also withdrew its rating for Avatar on Friday, after a call with company executives. While a rating withdrawal often portends insolvency for carriers, Petrelli said that Slide’s assumption of the homeowner book could help St. Johns survive. St. Johns is one of the larger insurers in Florida, with more than 160,000 policyholders. The transaction must be reviewed by the Florida Office of Insurance Regulation, but the office may expedite the matter in light of the shrinking number of carriers willing to do business in the state. Petrelli said Avatar may also be able find some financial assistance, but more will be known in coming days. The St. Johns non-rating, following years of healthy financial scores, was the result of the company revealing that it would not have as much surplus on hand as the rating agency requires, Petrelli said. “Based on conversations with the company and seeing their plan of action going forward, we decided to withdraw the rating,” Petrelli said. St. John’s third-quarter 2021 quarterly statement shows the firm had $46 million in policyholder surplus. But since then, the financial picture has darkened, and the company said it would not have that much in the bank by the end of 2022. “They had a disastrous fourth quarter,” Petrelli said. It’s unclear at this point what effect the takeover by Slide, and the non-rating of Avatar, will have on policyholders. Executives with the Orlando-based St. Johns and with the Tampa-based Avatar could not be reached for comment Friday. Petrelli said the Avatar rating withdrawal may not affect existing policyholders with mortgages, unless Avatar is put into liquidation by state regulators. Short of insolvency and liquidation, Florida’s Office of Insurance Regulation can take other steps, including agency supervision, to manage distressed companies. A spokeswoman for the office said OIR is working closely with St. Johns and Avatar “to facilitate options for consumers so they have continuous access to coverage.” Petrelli noted that St. Johns still has some amount of reserve funding. “The question is, how does it manage its reserves,” he said. The rating withdrawals are the starkest indication yet that Florida’s property insurance market is in meltdown, insurance industry leaders and state officials said this week. The industry has blamed hurricane losses, unnecessary and even fraudulent roof-replacement claims, and excessive litigation over claims. Insurance groups have urged Florida lawmakers to pass a new round of legislation that could help stem the red ink. The most comprehensive bill, SB 1728, was approved Wednesday by a key Senate subcommittee, and now goes to the full Appropriations Committee. The bill, by Sen. Jim Boyd, R-Bradenton, would allow insurers to write more policies that cover only the actual cash value of roofs, not full replacement value, except for damage due to a named hurricane. The bill also would attempt to limit solicitation by roofing contractors promising “free roofs” paid for by insurance companies, even when damage is from age and normal wear and tear. |

{kind=link}

Personal Service at Internet Prices!

|

|

|

© Olson & DiNunzio Insurance Agency, Inc., 2008

2536 Northbrooke Plaza Drive; Naples, FL 34119

Doing Business in the State of Florida

P: 239-596-6226; F: 239-596-1620; E: info@olsondinunzio.com

Featuring the cities of Naples, Bonita Springs, Marco Island and Estero Florida. Providing them the highest quality insurance and unbeatable rates.

Insurance Website Design